Why the RM vs NM Debate Isn't as Simple as Many Champagne Lovers Think

I recently read an article, written with passion and knowledge, celebrating the rise of Grower Champagne. The author defined Grower Champagne as "the small-estate stuff (you know, the ones with an RM on the back label)" and contrasted these artisanal wines with the supposedly faceless world of the Négociant-Manipulants, identified by the letters NM.

Like many champagne enthusiasts, I share the admiration for the growers behind the RM designation. Their stories are often fascinating, their connection to the land is tangible, and many produce outstanding wines.

What concerns me, however, is the increasingly common assumption that RM automatically means authentic and high-quality, while NM implies something less worthy of attention.

The reality is far more nuanced.

In many cases, the distinction between RM and NM tells us surprisingly little about the people making the wine, their values, or even the quality of the champagne in the bottle.

To understand why, it helps to consider the challenges faced by family-owned champagne producers.

1. Growth Is Essential for Survival

Every business needs to generate sufficient profit to survive. For family-owned champagne producers, the pressure can be particularly intense. Many estates have been passed down through several generations, and no one wants to be remembered as the person who presided over the decline of a family enterprise.

For younger vignerons taking over from their parents, there is often a natural ambition to grow the business. But this immediately creates a challenge.

An RM producer can only make champagne from grapes grown on vineyards owned by the family. In practical terms, this means that production is limited by the number of hectares they own and by the annual yield from those vineyards.

If demand grows, how can they increase production?

2. Buying More Vineyards Is Rarely Realistic

The obvious answer is to acquire more vineyards.

In practice, this is easier said than done.

Very little vineyard land changes hands each year. In 2025, only around 210 hectares were sold in a region containing approximately 34,000 hectares of vineyards.

Even when land does become available, the cost can be prohibitive. Champagne vineyard prices are among the highest in the world, the minimum in 2025 was €860,000 per hectare.

For most family-owned producers, expanding through vineyard acquisition is simply not a realistic option.

3. Becoming an NM Can Be the Natural Next Step

Another possibility is to stop selling grapes to the major houses and instead retain the entire harvest for the producer's own label.

Some growers do exactly this, but it involves considerable risk. Selling grapes under contract provides guaranteed income and predictable cash flow. Keeping every grape means waiting several years before the resulting champagne can be sold, while simultaneously finding new customers to buy it.

For many ambitious producers, a more practical solution is to purchase additional grapes from trusted growers.

To do this, they must obtain a Carte de Négoce, the licence that allows them to buy grapes from third parties. Once they do so, their legal status changes from RM to NM.

Yet what has actually changed?

The people making the wine have not changed.

The family history has not changed.

The philosophy of the estate has not changed.

The commitment to quality has not changed.

In many cases, the producer will work closely with the growers supplying the grapes and may exercise significant influence over how those vineyards are managed to ensure quality standards remain consistent.

The same family that was celebrated as an RM producer last year may be classified as an NM producer this year, even though almost everything that matters remains exactly the same.

La Famille Penet is a case in point. The family history goes back 4 centuries; their 6 hectares of family-owned vineyards are in the Grand Cru villages of Verzy and Verzenay – some of the best quality grapes you can find from which a range of fabulous single vineyard and blended champagnes are made, but there are only 6 hectares.

When Alexandre Penet took over responsibility for the family business a few years ago, he realised that becoming an NM was the only way to grow. Accordingly, he has been able to expand the range using the same winemaking philosophy as before – no malolactic fermentation, very low or zero dosage, long ageing and use of a perpetual reserve.

Look Beyond the Letters

The RM and NM classifications serve a useful regulatory purpose, but they are not a reliable guide to quality, authenticity or craftsmanship.

There are exceptional RM champagnes and mediocre RM champagnes.

There are exceptional NM champagnes and mediocre NM champagnes.

The letters on the back label tell us something about the legal structure of a business. They do not tell us everything about the people behind it, the care that went into the wine, or the quality in the glass.

For champagne lovers, the lesson is simple: don't stop your investigation at two letters on a back label. The most interesting stories — and often some of the best wines — are found by digging a little deeper.

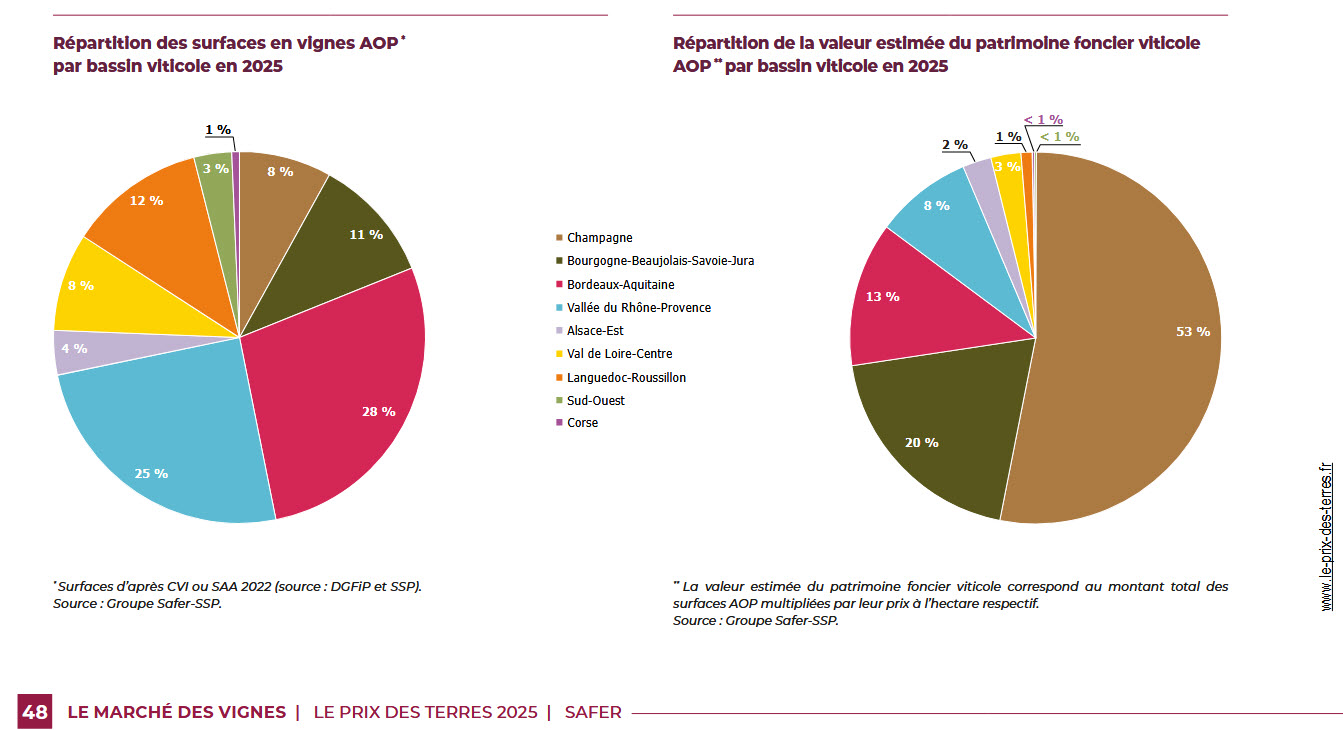

Even more striking is the fact that the report reveals that Champagne represents just 8% of the total surface area of vineyards in France, yet accounts for 53% of the total value of vineyard land in France!

Even more striking is the fact that the report reveals that Champagne represents just 8% of the total surface area of vineyards in France, yet accounts for 53% of the total value of vineyard land in France!

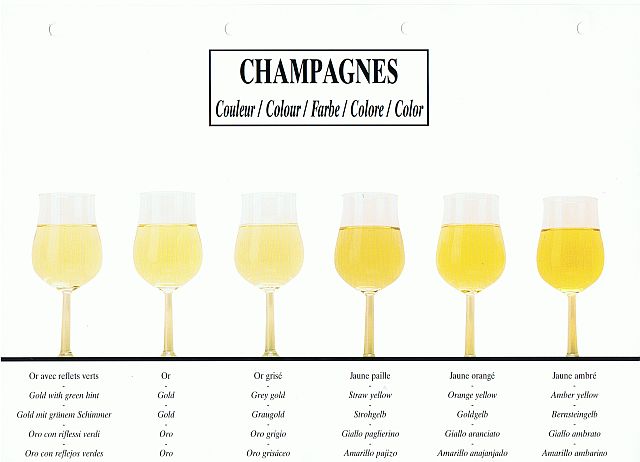

If you keep your bottle of champagne for any considerable length of time, it will gradually lose a little of its sparkle over the course of many years, and the colour will evolve from the youthful tones of pale yellow and gold towards the darker hues of copper and old gold.

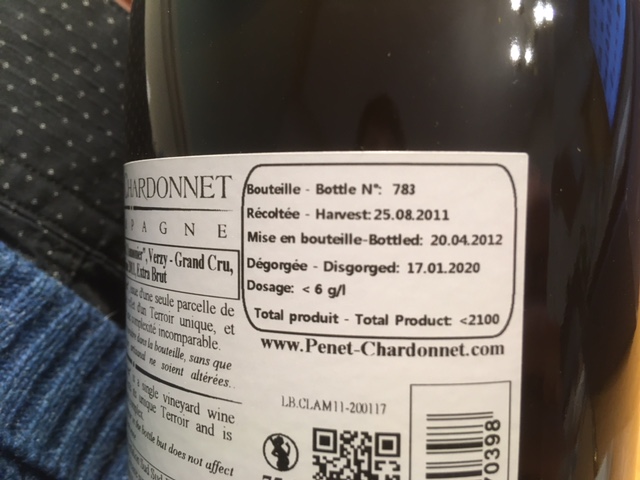

If you keep your bottle of champagne for any considerable length of time, it will gradually lose a little of its sparkle over the course of many years, and the colour will evolve from the youthful tones of pale yellow and gold towards the darker hues of copper and old gold.  To get around this problem and to assist anyone who wants to know more about the champagne they are drinking, an increasing, but regrettably still small, number of champagne makers print the disgorging date on the back label of the bottle.

To get around this problem and to assist anyone who wants to know more about the champagne they are drinking, an increasing, but regrettably still small, number of champagne makers print the disgorging date on the back label of the bottle. Ageing on lees refers to the time after the various wines have been blended by the champagne maker and put into bottles. Before the bottles are sealed a small amount of yeast and a small measure of sugar are added to produce the second fermentation inside the bottle during which the yeast cells are consumed by the fermentation and sink to the underside of the bottle where they form a sediment known as ‘the lees’.

Ageing on lees refers to the time after the various wines have been blended by the champagne maker and put into bottles. Before the bottles are sealed a small amount of yeast and a small measure of sugar are added to produce the second fermentation inside the bottle during which the yeast cells are consumed by the fermentation and sink to the underside of the bottle where they form a sediment known as ‘the lees’. The last component of the cap is what is called the ‘bidule’ which when translated, means simply ‘whatchamacallit’ or ‘widget’. It’s a small plastic shape that is designed to catch the lees when the bottle is turned neck-down at a later stage of the champagne making process.

The last component of the cap is what is called the ‘bidule’ which when translated, means simply ‘whatchamacallit’ or ‘widget’. It’s a small plastic shape that is designed to catch the lees when the bottle is turned neck-down at a later stage of the champagne making process. From that perspective it makes sense to leave the champagne to age on lees for as long as possible, but every bottle that is ageing in the cellars is a bottle not yet sold and they have to be financed, so a balance has to be found between the need to generate revenue by selling the bottles and the need for the champagne to be of high quality.

From that perspective it makes sense to leave the champagne to age on lees for as long as possible, but every bottle that is ageing in the cellars is a bottle not yet sold and they have to be financed, so a balance has to be found between the need to generate revenue by selling the bottles and the need for the champagne to be of high quality.